Business

‘I invested In A Ponzi Scheme’: Nigerians Fall Victim To Crypto Scams

Experts say financial illiteracy, lax regulations, greed and economic hardship make people susceptible to scam companies.

Lagos, Nigeria — Mandela Fadahunsi, who works at a technical training school in Ikeja in Nigeria’s Lagos, never believed he could fall victim to a Ponzi scheme.

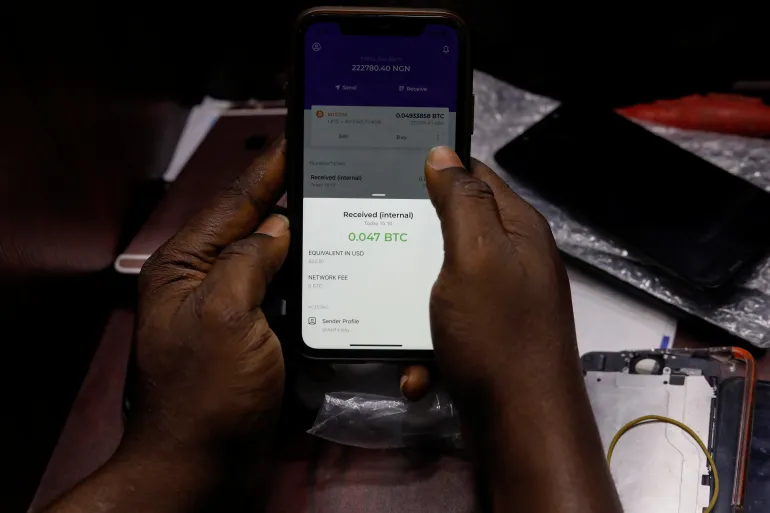

On April 6, the 26-year-old was starting his day when a WhatsApp notification lit up his phone screen. Someone on the group chat for investors of the cryptocurrency investment platform, Crypto Bridge Exchange (CBEX), had tried and failed to withdraw some funds, so they wanted to confirm if it was a general issue. Fadahunsi quickly logged on to his digital wallet and tried to withdraw 500 USDT, a cryptocurrency that stands for United States Dollar Tether, or simply Tether.

But 24 hours later, a process that should have taken just 10 minutes was yet to complete. He knew then that something had gone wrong. He started to panic, but half-hoped it was just a glitch or a minor system error.

“They [CBEX administrators] said it was as a result of the excessive volume of people trying to withdraw, and that all withdrawals have been placed on hold until 15th of April,” Fadahunsi told Al Jazeera.

On the 15th, he and fellow investors waited but heard nothing. On subsequent days, the administrators gave more excuses until the site stopped working altogether, and everyone’s money disappeared without a trace. That is when he realised he had been scammed and might never be able to recover the 4,596 USDT stablecoin in his wallet.

While Fadahunsi tallied his losses, the issue went viral on social media platforms.

Many more Nigerians shared their stories of loss, while others mocked them for losing their money to scammers. Some members of the public, filled with rage, attacked and ransacked CBEX offices in Ibadan and Lagos.

CBEX launched operations in Nigeria in July 2024, claiming to be able to generate immense trading profits using generative artificial intelligence. By January, it had gained serious popularity through referrals and smart advertising.

Fadahunsi and thousands of other people invested with the hope of making a maximum profit – the scheme promised up to 100 percent return on investment after a 40- to 45-day maturation period. At the start, the scheme did pay out, and the testimonies of successful initial investors attracted more people to sign up.

But after nine months of operation, the music stopped as the platform made away with an estimated 1.3 trillion naira ($840m), according to the official Nigerian Financial Intelligence Unit (NFIU). It left investors stunned.

Nigeria’s anticorruption agency, the Economic and Financial Crimes Commission (EFCC), has since labelled CBEX a Ponzi scheme. Experts say the organisers of such scams usually promise to invest people’s money in something that generates high returns, but in reality, it is investment fraud that pays existing investors with funds collected from new ones. Once a large number of people cash out, and new investors into the scheme dry up, it collapses.

Ponzi schemes, including CBEX, are usually not backed by any discernible economic activity, experts say. According to Ikemesit Effiong, from the Lagos-based socioeconomic advisory firm, SBM Intelligence, most times these businesses do not have anything to sell and have no recognisable business models. Even the agriculture-based ones claim to have products that investigators are unable to track. They also largely rely on existing investors to bring in new investors who serve as their downlink in the pyramid scheme.

Experts say that in Nigeria, widespread financial illiteracy, lax regulations, greed, economic hardship and peer pressure make investors susceptible to the machinations of Ponzi organisations that combine aggressive advertising, word-of-mouth campaigns charged by incentives, and initial high returns.

But at the end, the schemes leave victims – many of whom invest their savings, business capital, and borrowed money – unable to do anything but watch their hard-earned money disappear.

‘Make some gains’

Fadahunsi first heard about the CBEX scheme from colleagues at the start of the year. Initially, he was hesitant. But a few days later, his neighbour also mentioned the platform. Recognising that his close associates were participating, and not wanting to miss out, he decided to invest.

“I also thought the money was just sitting in my account, and it could be somewhere where I can make some gains on my money,” he explained.

In early February, he dipped into his rent savings and withdrew the entire 800,000 naira ($517). With that, he bought 500 USDT from the crypto exchange platform Buybit, receiving the coin in his digital CBEX wallet.

Four times a day on the CBEX platform, administrators dropped a code, which they call a “signal”. Investors were required to copy and paste the code into a section of their portal within the hour. CBEX said AI would then use that to make a trade, basically to buy and sell or change positions in such a way that it made a profit from price fluctuations on the investors’ behalf. Each time Fadahunsi pasted in the code, he would get 4.7 to 5 USDT as a profit, all of which accumulated towards his returns.

“So the more you do it, the more the percentage increases. In a month, I got double of 500 USDT,” he said, adding that there were also bonuses for things like referrals.

In March, users said CBEX made an adjustment where they no longer input the signal. Instead, investors just had to turn on an “AI hosting” option at the start of the day. But some investors say this was likely just a ploy to keep them going, to convince them they were still making a profit before everything crashed in April.

While some investors withdrew their returns, by the time CBEX crashed, Fadahunsi had not withdrawn any money. He had wanted to maximise the investment opportunity, to leave the funds to grow for five to six months before using them to buy a plot of land to build his future home. Now, that dream is dead.

“It is very hard, but thank God that my landlord is actually understanding,” he said.

“I am not proud of opening my mouth [to say] that I actually invested in a Ponzi scheme,” he lamented. “If I wasn’t greedy, I should have been able to withdraw two to three times on the platform, and it would have been successful.”

The USDT that CBEX invested in is a stablecoin pegged to the US dollar [File: Afolabi Sotunde/Reuters]

A history of Ponzi schemes

Even before CBEX, Ponzi schemes were not new in Nigeria.

In March, Nigeria’s anticorruption agency published a list of 58 Ponzi schemes presently operating in the country, and advised the public to “be vigilant and proactive”. This highlights the widespread presence of fraudulent entities masquerading as legitimate businesses in the country: in 23 years, Nigerians lost 911 billion naira ($589m) to Ponzi-related scams, the National Deposit Insurance Corporation (NDIC), which protects the country’s banking system, said in 2022.

Often, Ponzi schemes are able to operate by leveraging grey areas, such as obtaining an irrelevant certification that exaggerates their significance or legitimacy.

CBEX, for instance, obtained the EFCC’s anti-money laundering certificate through the corporate identity of ST Technologies International Ltd, and paraded it as a kind of clearance for conducting business.

However, the NFIU said CBEX was never granted a registration by the Securities and Exchange Commission (SEC) to operate as a Digital Assets Exchange, solicit investments from the public or perform any other function within the Nigerian capital market.

Legitimate businesses can be verified by checking the SEC website. However, experts say the vast majority of those who invest in shady schemes seem unaware or uneducated about this – 38 percent of Nigerians are financially illiterate, according to a 2023 central bank report.

At the same time, other victims may be willing participants, at least at first.

Joachim MacEbong, a senior analyst at Stears, a Lagos-based financial advisory firm, said while some victims are unwitting, others intentionally walk into Ponzi schemes hoping to make a quick profit before it crashes.

“There are those who know it is a scam, but they always feel they could cash out before everybody else. And so they would make that calculation, and it is largely because of the situation in the country; there is a lot of hardship. This kind of hardship increases the people’s desire to take risks and gamble with their very important funds,” he explained.

Nigeria’s economy has been on a downward spiral for decades, and is worse now that the country is going through its toughest economic downturn in about 30 years. Food prices have soared, and basic amenities are becoming inaccessible as the inflation rate sits at 23.71 percent. Against this backdrop, some see Ponzi schemes as a fast way to break out of the vicious cycle of poverty.

Like the proverbial early bird, early investors benefitted from the CBEX scheme, multiplying their returns for several months. Although social media is agog with complaints and bitter disappointment, some people said they had been able to make major purchases such as land and cars from their investment.

“The time scale at which you enter the investment will determine whether it will be a good investment or you will be a victim,” said Effiong of SBM Intelligence, but he added that many new investors are unaware of this catch.

‘We had a lot of plans’

Waris Oyedele is one of the people who invested their savings in CBEX because of worsening financial hardship in the country.

When he realised that the investment had crashed, he wept.

The 25-year-old comes from a low-income family. He graduated from Obafemi Awolowo University last year, but when he could not get a job, he started working as a shoemaker.

In January, he invested his savings of 800,000 naira (500 USDT); by March he had made 1,200 USDT.

He gave the returns to his younger brother to reinvest to help him pay for his future university studies, and in doing so, help ease their father’s financial burden.

“I felt bad [when we lost the money] because we had a lot of plans on it,” Oyedele said.

“I had a plan of buying a computer and going into UI/UX. Now it has gone.”

He is deeply affected by the situation and has reduced the way he spends his tiny income as he tries to rebuild his savings for future use and to support his brother.

Ponzi schemes play on psychology and human instincts by making it seem as though easy money is within reach, Effiong of SBM said.

All investments involve some form of greed, Effiong explained, and the promise of ending up with a higher return is one of the most elementary forms of human motivation: we all want more and as quickly as possible.

“What [a Ponzi scheme] does is that it also unlocks the deep-seated psychological bend for human beings to join groups – the obvious fear of missing out,” he said. “It also thrives on really aggressive marketing – all of that is to prey on the psychology of potential investors to not slow down.”

Agile tactics

Over the years, Ponzi schemes have employed several techniques to appeal to people, even going the extra mile to try and build public trust and goodwill. CBEX, for example, organised a sports competition and ran scholarships for schoolchildren to throw off suspicion, experts said.

In Nigeria, schemes rely heavily on existing investors who are incentivised to introduce new investors. They also engage in aggressive marketing using local and social media, sometimes involving radio, influencers and celebrity endorsements. Afrobeats stars Davido and Rema are some of the most popular celebrities to have unknowingly endorsed and made promo videos for Ponzi schemes in the past.

Ponzi schemes are also becoming increasingly sophisticated and dynamic as they leverage the latest technologies and digital tools, experts say.

“Many of them have apps with wonderful user experiences, which lend an air of credibility to their enterprise. Many of these scammers go to great lengths to design their products in such a way that they look and appear credible,” Effiong said.

MacEbong from Stears agreed, saying fake news and misinformation campaigns will become supercharged using AI tools, making it easier to hoodwink unsuspecting victims.

“There are numerous examples of generative AI being used to fool people who are even well informed and more savvy. When you turn these various tools against people with much lower exposure and information, they are practically defenceless,” MacEbong explained.

Regulators such as the SEC must become more proactive and come up with agile tactics to rein in Ponzi schemes and protect the public from illegitimate enterprises and shut them down before they cause harm, experts told Al Jazeera.

Businesses must be registered and thoroughly vetted because Ponzi schemes have been erroneously certified in the past, Effiong emphasised.

“There has to be a lot of financial education. Financial literacy is critical, which goes beyond how to make money, but [also] to educate the public on the tell-tale signs of Ponzi schemes. The responsibility also lies with the general public to educate themselves. If it sounds too good to be true, chances are it is too good to be true,” he said.

On May 26, EFCC said it had recovered a portion of the money stolen by CBEX and arrested two individuals promoting it. Al Jazeera tried to contact CBEX for comment through its website and publicly available phone numbers, but all were unavailable or out of service.

Meanwhile, many investors like Fadahunsi have lost hope and believe that the money they invested is all gone.

“Whatsoever the authorities retrieve, I am sure that nothing is going to come to me; I moved on already,” he said. “That is a very tough lesson for me. [Now,] I would rather keep my money in my account and spend it till the last dime.”

Aljazeera.com

The UK Home Office has set out detailed requirements that foreign nationals, including Nigerians, must satisfy before they can qualify for a Skilled Worker visa.

The requirements, published on the UK government’s official website, apply to overseas professionals seeking to work in eligible jobs with approved employers across the United Kingdom.

According to the Home Office, applicants must meet employment, salary, language and documentation requirements before a visa can be granted. Additional evidence may also be requested depending on an applicant’s circumstances.

1. Have a job offer from an approved employer: Applicants must first secure a job offer from a UK employer licensed by the Home Office to sponsor foreign workers.

The employer must issue a Certificate of Sponsorship (CoS), which contains details of the job being offered.

2. Work in an eligible occupation: The job must appear on the UK’s list of eligible occupations for the Skilled Worker visa. Applicants must know the correct occupation code assigned to their role before applying.

3. Meet the minimum salary requirement: Most applicants must earn at least £41,700 per year or the “going rate” for their occupation, whichever is higher.

Most applicants must earn at least £41,700 per year or the “going rate” for their occupation, whichever is higher. Lower salary thresholds may apply for some healthcare workers, graduates, younger applicants and certain PhD holders.

4. Prove English language ability: Applicants must show they can speak, read, write and understand English. This can be done through approved English language tests or recognised educational qualifications taught in English.

5. Hold a valid passport: Applicants must provide a valid passport or another accepted document proving their identity and nationality as part of the visa application.

6. Show proof of financial support: Most applicants must demonstrate they have at least £1,270 available to support themselves after arriving in the UK unless their employer confirms it will cover those costs.

7. Pay visa fees and healthcare surcharge: Applicants must pay the visa application fee, the Immigration Health Surcharge for each year of their stay, and meet any other required charges before their application can be processed.

Partners and children of Skilled Worker visa holders may apply as dependants. Supporting a partner requires showing at least £285 in available funds, £315 for one child, and £200 for each additional child

8. Submit supporting documents: Applicants must provide supporting documents, including their Certificate of Sponsorship reference number, salary details, occupation code and employer information. Depending on individual circumstances, additional documents may also be required.

9. Provide extra certificates where required: Some applicants may need to submit additional documents such as tuberculosis (TB) test results, criminal record certificates, Academic Technology Approval Scheme (ATAS) certificates or proof of overseas qualifications.

10. Apply within the required timeframe: Applicants must submit their Skilled Worker visa application within three months of receiving their Certificate of Sponsorship from their employer.

The Home Office also advises applicants to complete identity verification and provide all required documents before a decision can be made.

Additional documents may be requested

The UK government stressed that meeting the eligibility requirements does not automatically guarantee visa approval. Immigration officials may request further documents or information to verify an applicant’s eligibility before making a final decision.

For Nigerians and other foreign professionals hoping to work in the UK, understanding these 10 requirements can help them prepare a stronger Skilled Worker visa application.

Full breakdown of the rules can be downloaded here.

Transport fares have started rising in parts of the country as the price of Premium Motor Spirit (PMS), popularly called petrol or fuel, climbed to as high as ₦1,400 per litre amid a fresh increase in the international price of crude oil, according to Naija News.

The development has triggered fresh concerns among commuters, commercial transport operators and small business owners, who fear that the increase will further worsen the country’s cost-of-living crisis.

Naija News reports that the latest increase followed a surge in global crude oil prices, with Brent crude rising above $100 per barrel amid renewed tensions in the Middle East and concerns over possible disruptions to global oil supplies.

Fresh loading data obtained from petroleum marketers showed that ex-depot petrol prices increased in parts of Lagos, Warri and Calabar.

In Lagos, A.A. Rano increased its ex-depot price from ₦1,275 to ₦1,279 per litre, while African Terminal, Ascon, Gulf Treasure, Integrated and T.Time raised their prices to ₦1,275 per litre.

Aiteo, Heyden and Nipco maintained their existing price of ₦1,275 per litre, while Emadeb reduced its price marginally from ₦1,278 to ₦1,274 per litre.

The Dangote Refinery, the country’s dominant petrol supplier, on Thursday resumed gantry loading of Premium Motor Spirit in naira after a week-long suspension.

The refinery, however, raised its ex-depot petrol price to ₦1,215 per litre.

It had suspended gantry and coastal loading on July 15 after introducing a dollar-denominated pricing template for its refined petroleum products.

The latest adjustment represents a ₦140 increase per litre, or a 13.02 per cent rise, from the previous price of ₦1,075 per litre.

The refinery had attributed the introduction of dollar-based transactions to difficulties in accessing enough crude oil under the Federal Government’s naira-for-crude arrangement.

Under the temporary dollar-based pricing system, petrol was sold at $0.779 per litre, diesel at $1.087 per litre and Jet A1 aviation fuel at $0.942 per litre.

Nigerians Lament Rising Transport Costs

Naija News reports that the fresh increase has sparked anger and frustration among Nigerians, with residents complaining that transport fares usually rise immediately after petrol prices go up but rarely fall when the cost of crude oil drops.

Before the latest escalation in Middle East tensions, Brent crude had fallen to around $70 per barrel, the level at which it traded before the war in February.

However, Nigerians said petrol prices remained above ₦1,000 per litre despite the drop in international crude prices.

The Federal Government had previously summoned oil marketers and other stakeholders to ensure that petrol prices reflected the decline in international crude prices. However, residents said there was no significant reduction before the latest increase.

In Abuja, residents said rising transport costs were taking a large portion of their monthly income.

A civil servant, Grace Okeke, who spoke with Daily Trust, said every increase in petrol prices immediately affected her cost of transportation.

“My salary has not changed, but I now spend much more just getting to work and back. It is becoming impossible to survive in Abuja,” she said.

Another resident, Musa Ibrahim, said the increase would also affect the prices of food and other essential goods.

“Transportation affects everything. Farmers, traders and transporters will simply transfer the additional cost to consumers. Ordinary Nigerians are the ones paying the price,” he said.

Drivers Struggle With Rising Fuel Costs

Commercial drivers said they were also facing difficulties as the price of petrol continued to change.

A taxi operator, Emmanuel Ujah, said the frequent changes made it difficult for drivers to plan their businesses.

“You don’t know what petrol will cost tomorrow. That uncertainty affects our business and our families,” he said.

Another driver, Ganiyu Jide, said fuel now takes the biggest part of his daily earnings.

“If we don’t adjust transport fares, we cannot maintain our vehicles or even feed our families,” he said.

Although transport fares have not increased uniformly across Abuja, commuters said they were paying between 20 and 40 per cent more on some routes compared with a few weeks ago.

In Lagos, some transport operators have started reviewing fares on busy routes.

However, competition among commercial bus operators has prevented a general increase across the state.

Fuel marketers are also selling petrol at different prices, depending on their location and source of supply.

The varying prices have created uncertainty for transport operators who often need to buy fuel more than once a day.

Ibadan Fares Remain Stable

In Ibadan, the Oyo State capital, transport fares have remained relatively stable despite petrol selling between ₦1,260 and ₦1,300 per litre at some filling stations.

BOVAS sold petrol at ₦1,260 per litre, while Amazing Filling Station dispensed the product at ₦1,300.

A commercial driver, Kamoru Iyanda, said transport operators could not increase fares every time petrol prices went up because passengers were also struggling.

“It is difficult to adjust fares every time because passengers cannot afford it. Sometimes we absorb the losses,” he said.

Another driver, Amoo Saheed, said unstable fuel prices had continued to reduce the earnings of commercial transport operators.

In Ilorin, Kwara State, several major and independent filling stations increased their pump prices by between ₦35 and ₦85 per litre.

AP raised its price from ₦1,220 to ₦1,290 per litre, while BOVAS and Abanik sold at ₦1,260.

NIPCO sold at ₦1,300, NNPCL stations at ₦1,305, Optimal at ₦1,255 and External at ₦1,298.

Shafa and Atgris sold at ₦1,300, Total at ₦1,285 and Olak at ₦1,260 per litre.

Residents said the increase would have a ripple effect on transport fares and the prices of food and other goods.

They urged the government and relevant agencies to take urgent steps to stabilise petrol prices and reduce the burden on ordinary Nigerians.

One resident, Ola Yemi, described the development as disturbing and criticised the government’s policies.

“It’s very disturbing, and some of the policies of this government are really disappointing. I am beginning to think seriously that it is because of the forthcoming election. I believe they are trying to raise enough funds without considering the condition of the masses.

“Initially, we were told that the increase was because of the tension in the Middle East, but the situation appears different now,” he said.

Kaduna drivers uncertain over future prices

In Kaduna, petrol was selling for about ₦1,350 per litre after dropping below ₦1,200 only a few weeks earlier.

A commercial driver, Hassan Ya’u Kanti, said the rapid changes in petrol prices were becoming unbearable.

“A few days ago we bought fuel at about ₦1,190. Now it is ₦1,350. We don’t know what tomorrow will bring,” he said.

He said passengers often blamed drivers whenever transport fares increased, despite the rising cost of fuel.

“We are only trying to survive,” he added.

Adamawa Operators Monitor Market

In Adamawa State, NNPCL stations were selling petrol at ₦1,310 per litre, while AA Rano, Eterna and other independent marketers sold between ₦1,360 and ₦1,370.

The Commercial Manager of Adamawa Sunshine Transport Company, Aminu Muhammad, said the company would study the situation before deciding whether to increase fares.

“We don’t rush into increasing transport charges. We usually monitor developments for several weeks before taking any decision,” he said.

Kano Fares Unchanged

In Kano, transport fares have remained largely unchanged despite the increase in petrol prices.

Commercial tricycle operators said they were waiting to see if the fuel price would stabilise before reviewing their fares.

A tricycle operator, Hayatu Usman, said the latest increase was not enough to justify an immediate fare hike.

Passengers interviewed in the city also confirmed that they were still paying the same fares.

A Bayero University Kano student, Mujahid Aminu, said he still paid ₦300 for his daily trip from Zawaciki to the university’s New Campus.

Maiduguri Transport Fare Rises By ₦5,000

In Maiduguri, Borno State, independent filling stations were selling petrol between ₦1,370 and ₦1,390 per litre.

The development has also affected inter-state transportation, with the fare from Maiduguri to Kano rising from ₦20,000 to ₦25,000.

The Chairman of the Independent Petroleum Marketers Association of Nigeria in Borno State, Mohammed Kuluwu, said fluctuating prices were discouraging some marketers from buying petrol.

“Sometimes you buy at a high price only for prices to fall before the product reaches Maiduguri. Many marketers are now afraid to buy,” he said.

Small business owners who depend on petrol-powered generators also expressed concern over the latest increase.

A barber, Chinedu Nwafor, said he was spending more on petrol for transportation and electricity generation.

“If this continues, I will have no option but to increase the prices of my services,” he said.

Market Forces To Blame – Says Expert

An energy law expert at the University of Lagos, Professor Dayo Ayoade, said the rising petrol prices were a reflection of Nigeria’s deregulated petroleum market.

He explained that local petrol prices were now directly affected by movements in international crude oil prices and the exchange rate.

According to him, the Petroleum Industry Act limits government intervention in petrol pricing except when there are market anomalies.

However, he said Nigeria’s crude oil commitments under existing financing arrangements had reduced the volume of crude available for domestic supply.

He said, “When price of crude oil is high, that price will be passed on to consumers. You can see that Dangote at one point was talking about Nigerian marketers paying for its products in dollars because the vast majority of its expenditure is in dollars and it’s spending a lot of money to import crude oil into Nigeria. This means that the crude oil for Naira has, I don’t want to say failed, but it has been of limited use to Dangote refinery.”

He added, “As such, we find that the exposure of our local PMS markets to the vulnerabilities of an oil shock and increasing prices due to the US-Iran war will be ongoing. So long as the war continues, the price will go up and Nigeria will be unable to protect itself against that higher cost.”

Ayoade said the government and the Nigerian Midstream and Downstream Petroleum Regulatory Authority (NMDPRA) had limited capacity to protect consumers from the impact of rising crude oil prices.

“The Petroleum Industry Act provides for a market price, so it’s the market that now determines the price in Nigeria. Unfortunately, the federal government and NMDPRA have limited capacity to intervene and insulate consumers from crude oil.

“One way we could have done it is to expand Naira for crude, but if you go and check, Nigeria has mortgaged the overwhelming majority of its crude oil cargoes for cash and because it has done this, the amount of barrels available is so small and that it’s embarrassing,” he said.

Another industry analyst, Abdullahi Shehu, called on the Federal Government to subsidise crude oil supplied to the Dangote Refinery and other local refineries.

“He can subsidise ₦700 per litre to all the local refineries so Nigerians can buy petrol at ₦500 per litre. This is better for Nigerians than seeing the savings from subsidy removal being looted mercilessly,” he told Daily Trust.

An economist and oil and gas expert, Dr Marcel Okeke, also said the government’s reforms were not producing the desired results.

According to him, any reform that fails to improve the welfare and standard of living of citizens cannot be considered successful.

He said, “The truth is whatever you claim you have achieved and it doesn’t reflect in the well being, welfare and standard of living of the people, what are you talking about?

“Many Nigerians have been made worse off by the reforms. Look at the situation of petrol alone, as of May 2023, the price per litre was below N200 per litre. At that time it came to N800. But since the Middle East war started, everything has gone haywire, moving around N1,300 and N1,400 and now it is going to N1,500.”

Okeke alleged that the government had failed to fix the country’s refineries and reduce dependence on imported petroleum products.

He attributed the failure to what he described as vested interests benefiting from fuel importation.

“They want to continue the importation so as to continue the super profits they are making,” he said.

Source: Naija News

Adefunke Kuyoro, a former president of the Association of Professional Party Organisers and Event Managers of Nigeria (APPOEMN), is dead. Kuyoro’s death was confirmed in a statement released by the deceased’s family.

Legit.ng learnt that Kuyoro, 64, “peacefully transitioned to glory”.

Kuyoro’s company, TWC Events Services, also confirmed the sad update. TWC Events’ statement, jointly released by the Kuyoro family, read

“It is with a heavy heart that we, the TWC Event Management Services, announce the passing of our beloved CEO, Mrs. Adefunke Kuyoro, fondly known to us all as Mummy K/Mrs. K.

“Mummy K was not just our leader; she was our pillar, our inspiration, and the heart of everything we built together.

Her grace, vision, and passion for excellence defined TWC Event Management Service, and her impact will live on in every event we ever touch.

“We are devastated by this loss, but we are comforted knowing that she lived a life full of purpose, love, and dedication.”

The statement added: “To everyone who has reached out with condolence messages, calls, and kind words, the family and the entire TWC team are deeply grateful. Your love and support during this incredibly difficult time means more than words can express.

Thank you from the bottom of our hearts. “Mummy K, you will forever remain in our hearts. Rest in perfect peace.”

A Facebook post on Adefunke Kuyoro confirming the entrepreneur’s demise can be viewed:

SHOCKER! Sheikh Gumi Mentions Two Top Nigerian Leaders Who Visited Militants

2027 Election: Tinubu’s Ex-Minister Adelabu Speaks On Dumping APC

UK Lists 10 Requirements Nigerians Need To Secure Work Visa

Former Super Eagles Star Loses Life Savings, Duped By A Pastor of ₦1.2 Billion

I’m A Married Man, I Can Never Get Myself Involved With Such A Thing, Delta Gov Aide Reveals Why He Offered Comfort ₦500,000 Job

Lagos Imposes ₦250,000 Fine For Illegal Waste Disposal

-

Politics2 days ago

Politics2 days agoFULL LIST: APC Uploads 13 Governorship Candidates to INEC Portal

-

Business2 days ago

Business2 days agoNo More N1300/liter: Petrol Stations Release New Fuel Prices Nationwide

-

Tech20 hours ago

Tech20 hours agoBREAKING: Painful, APC Chairman Bereaved

-

Business2 days ago

Business2 days agoBREAKING: Tears as Top Nigerian Buśineśś Icon Passes Away

-

Entertainment2 days ago

Entertainment2 days agoBBNaija Season 11 Returns With Bigger Prize, Twists [All You Need To Know]

-

Politics15 hours ago

Politics15 hours ago2027 Election: Tinubu’s Ex-Minister Adelabu Speaks On Dumping APC

-

Entertainment2 days ago

Entertainment2 days ago‘Woman’s Financial Status Doesn’t Matter To Me’ – Singer Ruger

-

Entertainment2 days ago

Entertainment2 days agoFrom Stage To Style: Davido Sets The Standard In Royal Blue